RESIDENTIAL STATUS

.~ RESIDENTIAL STATUS ~.

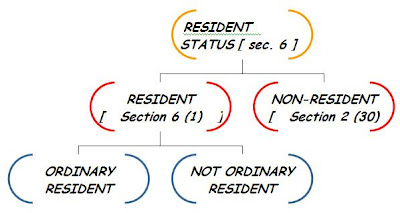

The residential status of different types of persons is determined differently. Similarly, the residential status of the assessee is to be determined each year with reference to the “previous year”. The residential status of the assessee may change from year to year. What is essential is the status during the previous year and not in the assessment year.

Residential Status-:

*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~

*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~*~

1. Resident-:[ Section 6 (1) ]

To determine the residential status of an individual, section 6(1) prescribes two tests. An individual who fulfils any one of the following two tests is called Resident under the provisions of this Act. These tests are-:

(a) If he is in India during the relevant previous year for a period amounting in all to 182 days or more.

OR

(b) If he was in India for a period or periods amounting in all to 365 days or more during the four years preceding the relevant previous year and he was in India for a period or periods amounting in all to 60 days or more in that relevant previous year.

Explanation—(a) In case of individual being a citizen of India who leaves India in any previous year as a member of the crew of an Indian ship is defined in clause (18) of section 3 of the Merchant Shipping Act 1958 (44 of 1958) or for the purposes of employment outside India the provisions of sub-clause (b) as given above shall apply in relation to that year as if the words “sixty days” have been substituted by “182 days”.

(c) (b) In case of an individual being a citizen of India, or a person of Indian origin with in the meaning of explanation to clause (e) of section 115 C, who being outside India , comes on a visit to India in any previous year, the provisions of sub-clause (b) shall apply in relation to that year as if for the words. ‘ sixty days occurring there in the words ONE HUNDRED AND EIGHTY TWO DAYS had been substituted.’

2.Resident but not ordinarily Resident-:[section 6(6) ]

An individual who is resident u/s 6(1) can claim the beneficial status of N.O.R if he can prove that:

(a) He was non resident in India for 9 previous years out of 10 previous years preceding the relevant previous year.

OR

(b) He was in India for a period or periods aggregating in all to 729 days or less during seven previous years proceeding the relevant previous year.

3. Non-Resident-:[ Section 2(30) ]

Under section 2(30) of the Income –tax Act, 1961 an assessee who does not fulfil any of the two conditions given in section 6(1)(a) or (b) would be regarded as ‘Non-Resident’ Assessee during the relevant previous year for all purposes of this Act.

Like it on Facebook, Tweet it or share this article on other bookmarking websites.